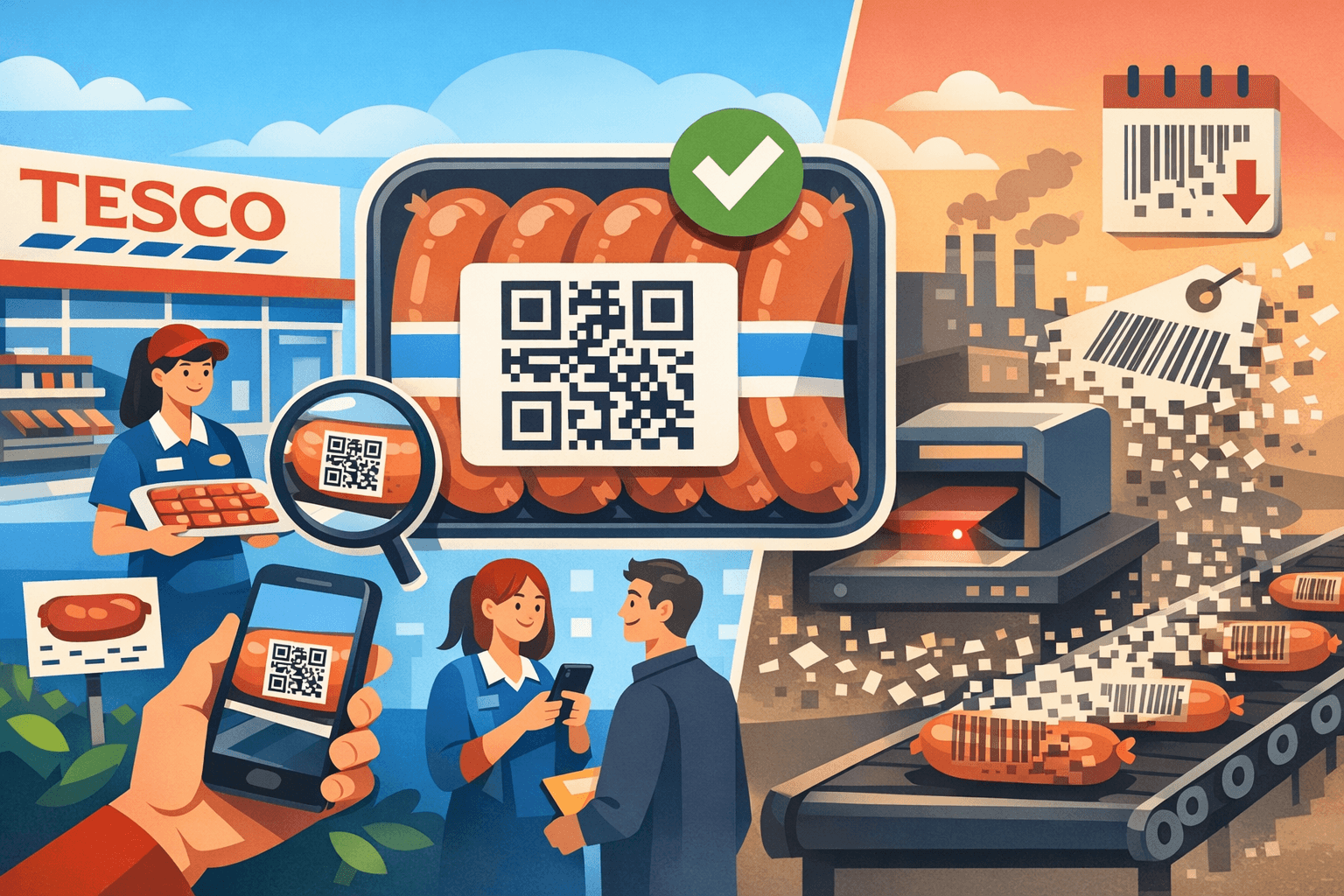

British supermarket giant Tesco is quietly running a live experiment in how far shoppers are willing to go to scan their sausages.

In a trial across around 30 stores, Tesco has started replacing familiar black-and-white barcodes with QR codes on meat packaging. Not just adding them — replacing them. It’s a small design tweak that hints at a much bigger shift: the old linear barcode, the thing that turned retail into a data industry in the 1970s, is finally being unseated. And for the world of product information management (PIM), this isn’t a packaging story — it’s a signal that the core identifiers we rely on for commerce are evolving in public, on the shelf, in real time.

Tesco’s QR test: what’s actually changing on the shelf

The trial is simple on the surface. Tesco has begun introducing QR codes on certain meat products as the primary scannable code. Instead of a traditional EAN/UPC barcode, the pack carries a QR that both tills and smartphones can read. In-store, that code acts as the price and inventory key. At home (or in the aisle), customers can scan the same code to access extra information.

That “extra information” is the key differentiator. A legacy barcode is essentially a numeric ID linked to a database. A QR code is a gateway: it can still carry that numeric ID, but it can also point to structured product data, extended content, and services. Think:

- Ingredients, allergens, and nutritional details beyond what fits on a label

- Batch-level traceability, including origin, processing plant, and transport chain

- Dynamic content like cooking tips, recipes, or storage guidance

- Regulatory disclosures that can be updated without reprinting the pack

For the average Tesco shopper, it may feel like a slightly more modern black-and-white square. For anyone working in PIM or master data, it’s the front end of a more ambitious architecture: a single scannable surface that connects the physical product to a constantly updated stream of product information.

Why retailers are finally serious about QR and 2D codes

The timing isn’t accidental. Global standards body GS1 has been pushing hard for a transition from traditional linear barcodes to more data-rich, “2D” codes like QR and DataMatrix, under the banner of the “Sunrise 2027” initiative. By around 2027, the goal is for 2D codes to be widely scannable at retail point-of-sale worldwide.

Tesco’s test is one of the most visible UK experiments aligned with this shift. It’s happening for three main reasons:

- Regulation is outgrowing the label. Food safety, sustainability disclosures, country-of-origin rules, and packaging legislation are demanding more-character-dense, sometimes dynamic information. A single printed panel can’t keep up.

- Shoppers now expect transparency. Post-pandemic, “where did this come from” is a mainstream question, not a niche one. Retailers are judged on traceability, ethics, and environmental impact — and need a scalable way to expose that data.

- Omnichannel APIs need a physical anchor. The same item now lives on the shelf, in an app, in click-and-collect workflows, and on marketplaces. A flexible, globally recognized scannable ID is the connective tissue between all those representations.

In that context, barcodes look like dial-up. They still work, but they weren’t built for this world.

What this means under the hood: PIM has to grow up

Swapping a barcode for a QR code is superficially about printing. In reality, it forces retailers and brands to answer a harder question: when a customer scans this code, what exactly do we show them, and where does that information live?

This is where product information management, long treated as a back-office necessity, becomes a frontline system.

From static attributes to living product records

Traditional PIM implementations in retail focus on core attributes: name, description, size, weight, images, some compliance notes. Enough to run a shelf label and a basic product page. QR-enabled packaging raises the bar.

To make good on the promise of a scannable code, PIM now has to handle:

- Multi-layered product hierarchies: item, batch, lot, sometimes even unit-level specifics

- Dynamic data: changed sourcing, reformulations, supplier switches, updated certifications

- Region-specific variants: different legal statements, languages, and marketing claims per market

- Connected content: recipes, videos, how-tos that need to be referenced and versioned

In short, the “product record” can no longer be treated as a static card. It’s now a living object connected to manufacturing systems (ERP/MES), supply chain platforms, DAM systems for media, and increasingly to sustainability and compliance data services.

Identity is the new battleground

QR codes also sharpen a long-simmering issue: who owns the canonical product identity, and what format does it take?

Correctly implemented, a 2D code can carry a GS1 Digital Link — essentially a standardized way to encode a product identifier (GTIN) plus optional parameters (batch, expiration, location) in a URL-style string. That string then resolves to product data.

That has two big implications for PIM:

- Product IDs have to be consistent and global. Local hacks (reused codes, duplicated SKUs, “special” IDs for promo stock) break when the customer’s camera becomes a global validator. PIM and ERP need a cleaner, more disciplined ID strategy.

- URL-level design matters. The QR is often encoding an HTTP endpoint. That forces retailers to think like API product teams: versioning, redirects, uptime, and what happens when that endpoint changes in five years.

This is why PIM strategy is quickly bleeding into areas you’d traditionally associate with API gateways, integration platforms, and even observability tooling. If the code on the pack is the entry point to your product information, that journey cannot fail.

How QR-enabled packaging collides with existing PIM stacks

Most enterprise PIM landscapes weren’t built for Tesco-style experiments at scale. They’re a patchwork: ERP as source of truth for some attributes, a legacy PIM for others, marketing clouds for imagery, and a handful of bespoke integrations in between. Layering dynamic, scannable codes on top of that exposes the cracks.

Key friction points emerging in the market

- Data governance gaps. Who is allowed to change what a QR leads to? Can a brand update allergy information in near real time — and how is that approved and audited?

- Batch- and lot-level detail. Many PIM setups treat “product” as a monolith. Food, pharma, and cosmetics increasingly need batch-level accuracy. That data often lives in ERP or LIMS, not PIM, yet the consumer-facing code has to reflect it.

- Latency and synchronization. If sourcing changes today, how long does it take for the new origin statement to appear behind that QR? Hours and days are no longer acceptable if regulators or public scrutiny are involved.

- UX fragmentation. Retailers risk spinning up one-off microsites for every format of QR campaign (loyalty, recipes, traceability). Without a PIM-centric content strategy, the experience quickly becomes incoherent.

These issues are pushing retailers and manufacturers back toward a hard question the PIM industry has dodged for years: where does product truth really live, and how do we expose it in a way that both systems and humans can consume reliably?

What the Tesco trial signals for PIM vendors

For software vendors, Tesco’s move is not just a marketing-friendly anecdote; it’s commercial pressure. The shift to 2D codes at retail is forcing PIM platforms to evolve in at least four directions.

1. From internal tooling to consumer-facing infrastructure

PIM used to live in a comfortable, mostly invisible layer between ERP and e-commerce. With QR codes as direct customer entry points, PIM data is now part of the front-end experience. That means:

- APIs that can handle consumer-scale traffic, not just nightly batch jobs

- Latency targets that look more like web performance SLOs than back-office SLAs

- Support for personalization and context (e.g., geo-based content, language, regulations)

Some vendors will lean into this and build tightly integrated “product experience” layers. Others will stick to being strong back-end data hubs and rely on composable stacks around them. The market is already bifurcating.

2. Tighter alignment with GS1 and Digital Link standards

The days when PIM vendors could treat identifiers as “just fields” are ending. Supporting GS1 Digital Link natively — understanding how GTINs, attribute vocabularies, and URL resolution fit together — is becoming table stakes for enterprise retail and CPG accounts.

Expect to see more PIM roadmaps talking about:

- Native management of Digital Link templates and resolution rules

- Built-in validation for GTINs and related identifiers

- Prebuilt connectors to GS1 services and national product registries

3. Event-driven PIM, not just workflow-driven PIM

QR-connected products create an expectation of “live” accuracy. When a supplier updates an origin, or a certification is revoked, the information behind the code should change rapidly. That requires event-driven architecture rather than slow, linear workflows.

PIM systems moving with the trend are:

- Emitting and consuming events for product changes in near real time

- Integrating with streaming platforms to propagate updates across channels

- Building more granular audit trails to show what the consumer saw at any given time

4. Deeper triangulation with ERP, DAM, and compliance systems

A QR code is a convergence point: pricing and inventory from ERP, imagery and video from DAM, specifications and constraints from PLM and compliance systems. PIM vendors who treat integration as an afterthought are going to struggle.

We’re already seeing a trend toward:

- Predefined connectors for major ERP suites to sync batch and lot attributes

- Native DAM capabilities or tight DAM integrations to serve approved media per product

- Hooks into regulatory content providers and sustainability data platforms

The common thread is that QR-driven use cases are exposing just how siloed many “single sources of truth” actually are.

Broader PIM market trends this experiment underscores

Tesco’s barcode swap is one trial, in one country, covering a narrow slice of SKUs. But it intersects with several broader trends shaping the PIM market over the next five years.

The product graph is getting denser

Products are increasingly defined not just by features, but by relationships: to suppliers, to certifications, to sustainability scores, to usage contexts, to localized variants. PIM is moving from flat attribute tables to graph-like structures.

2D codes and Digital Link fit neatly into this world: they don’t just point to “a product”, they can point to specific nodes in a product graph (this batch, in this region, under this regulatory regime). Vendors that can model and query that graph efficiently will have an edge.

Regulation-driven innovation, especially in food and pharma

Regulatory pressure — from provenance rules to extended producer responsibility to stricter labeling laws — is accelerating PIM investment more than pure marketing ambition. Tesco’s meat trial sits squarely in that space: traceability and compliance dressed up as convenience and transparency.

We’re likely to see similar moves in:

- Pharmaceuticals and medical devices: where serialization and track-and-trace are already mandatory in many markets

- Cosmetics and personal care: where ingredient disclosures and allergen information are under heightened scrutiny

- Household chemicals and DIY: where safety and disposal rules need more than a tiny printed icon

For PIM providers, this means compliance features are not niche add-ons; they’re core differentiators.

From “PIM as a project” to “PIM as infrastructure”

Tesco’s trial also reflects a maturing mindset. PIM can’t be treated as a one-off centralization project anymore. As product identities and code standards keep evolving, PIM becomes an ongoing, foundational capability — closer in spirit to an API platform or data mesh node than a static MDM installation.

Retailers and brands that accept this are reworking budgets and organization charts: dedicated product data teams, ongoing data stewardship, and continuous integration between PIM, ERP, DAM, and customer-facing channels. Vendors that rely on a “big bang implementation” mindset will find this new reality unforgiving.

The quiet end of the one-dimensional barcode era

The day Tesco printed its first pack of sausages with a QR code at the checkout instead of a barcode, it was also printing a future in which physical products are clickable by default. That future doesn’t work without PIM systems that can keep up — not just with more attributes, but with a different conception of what a “product” even is.

2D codes aren’t inherently radical; they’re just a denser way to encode information. But on the shelf, in front of millions of shoppers, they force long-delayed decisions about product IDs, data ownership, traceability, and the plumbing between all the systems that claim to be authoritative. If Tesco’s experiment looks mundane, that’s only because the hardest changes are happening off-label, in databases and APIs most people will never see.

For the PIM market, that’s the real story. The upgrade from stripes to squares is also an upgrade from catalog-era product data to something more alive, more interconnected, and much harder to fake. The supermarkets that figure this out first won’t just scan faster — they’ll know, and be able to prove, a lot more about everything they sell.

Source: https://www.independent.co.uk/news/uk/home-news/tesco-barcodes-qr-code-sausages-b2959572.html